Related Blogs

Table of Contents

- Can NRIs Invest in the National Pension System (NPS)?

- Key Takeaways

- What Is the National Pension Scheme (NPS)?

- As an NRI How to Invest in National Pension Scheme?

- Documents Required to Open an NPS Account for NRIs

- Eligibility Criteria for National Pension Scheme for NRIs

- Benefits of the NPS Pension Scheme for NRIs

- What Are the Investment and Withdrawal Options for NPS for NRIs?

- Conclusion

The National Pension System (NPS) is one of India's most trusted retirement savings schemes, regulated by the Pension Fund Regulatory and Development Authority (PFRDA). Although it was first introduced for government employees, today eligible Indian citizens, including Non-Resident Indians (NRIs), can also invest in it.

In this guide, we'll explain everything you need to know about the National Pension Scheme for NRIs, including eligibility, documents, investment process, tax benefits, and withdrawal rules.

Can NRIs Invest in the National Pension System (NPS)?

Yes. Eligible Non-Resident Indians (NRIs) can invest in the National Pension System (NPS) by opening an account through eNPS or an authorised bank. They can register using their PAN card, complete the KYC process, and link an NRE or NRO bank account. The National Pension Scheme for NRIs offers retirement savings, market-linked returns, tax benefits, and flexible investment options.

Key Takeaways

- Eligible NRIs and OCI cardholders can invest in the National Pension System (NPS), subject to the latest PFRDA guidelines.

- An NPS account offers market-linked returns, tax benefits, flexibility, and portability, making it a suitable long-term retirement option for many NRIs.

- Before investing, always check the latest eligibility, contribution, and withdrawal rules issued by the PFRDA, as they may change over time.

What Is the National Pension Scheme (NPS)?

NPS is a retirement saving scheme wherein an individual can earn returns on their investment. In addition, it creates an inflation-adjusted corpus that meets the financial needs of the individuals after their retirement. In this, you have to contribute a specific amount every year till its maturity. Once you reach retirement and complete the required withdrawal process, a part of your accumulated corpus is generally used to purchase an annuity, which provides a regular pension income. The remaining amount can be withdrawn as per the applicable NPS withdrawal rules. The NRI pension scheme is available to Indian citizens whether they are residents or not of the country. Hence, NRIs can also invest in the NPS scheme. Moving further, let's know how they can do so.

As an NRI How to Invest in National Pension Scheme?

Investment in the NPS for NRI can be done through visiting the online NPS website. In addition, you can also use the bank, which allows you to open an NPS account in your name. Moving ahead, let's know how to apply online for NPS through eNPS.

- First, visit the official website of eNPS

- There click on the "National Pension System" and then click on the "Registration" option.

- You will see a new page open on your window screen. From the field of "status of applicant", select the "non-resident of India" option.

- Through your PAN card number, you can register yourself for NPS for NRI online. Under the option "register with", select the option "permanent account number."

- Next, you need to mention the NRE or NRO bank account number, PAN card number, passport number, and your bank details.

- In addition, mention the name of the country you are currently living in.

- After mentioning all these details, click on the "continue" option.

- State the information related to your investment and choose the scheme and pension fund manager.

- With this, you also need to upload scanned copies of your documents along with your signature and photograph.

- Fill out the complete form and take a printout of it.

- Once you've completed the registration process, follow the verification steps as instructed during your application. Depending on the registration method you choose, the verification process may differ. Always follow the latest instructions provided on the official eNPS portal or by your authorised bank.

With this, by following the steps as mentioned above, you can register yourself for the NRI pension scheme. However, before applying for the scheme you need to fulfill some eligibility criteria fixed for NRI. Want to know what they are? Read the next section and get your answers.

Documents Required to Open an NPS Account for NRIs

Before you begin the registration process, it's a good idea to keep all the required documents ready. This makes the application process much easier and helps avoid unnecessary delays.

Generally, you'll need:

- A valid Indian passport

- PAN card

- NRE or NRO bank account details

- Recent passport-size photograph

- Signature

- Overseas address proof (if required)

- KYC documents as requested by your bank or Point of Presence (POP)

Depending on the bank or service provider, you may also be asked for a few additional documents during verification.

Eligibility Criteria for National Pension Scheme for NRIs

To invest in the National Pension Scheme, NRIs need some basic eligibility criteria. This includes the following things:

- Eligible individuals can join the National Pension System within the age limit prescribed by the Pension Fund Regulatory and Development Authority (PFRDA). Before applying, it's always a good idea to check the latest eligibility guidelines.

- Apart from that, you should have a valid bank account. It can be either a Non-Resident External (NRE) account (repatriable) or a Non-Resident Ordinary (NRO) account (non-repatriable).

- Fulfilling the KYC norms is also needed to open the NPS account for NRIs.

You should have a valid PAN card and complete the required KYC formalities while opening your NPS account. Eligible Indian citizens, including NRIs and Overseas Citizens of India (OCIs), can open an NPS account subject to the applicable PFRDA guidelines. However, Persons of Indian Origin (PIOs) are not eligible. If an NRI or OCI loses their eligible status under the applicable regulations, the NPS account will be governed according to the prevailing rules.

These are the eligibility criteria as an NRI you need to follow to apply for the NPS scheme. Applying to this scheme secures your future. In addition, it offers you a fixed source of income after your retirement. With this, there are lots more perks that NPS for NRI provides to individuals. Want to know about them? Browse to the next section and get your answers.

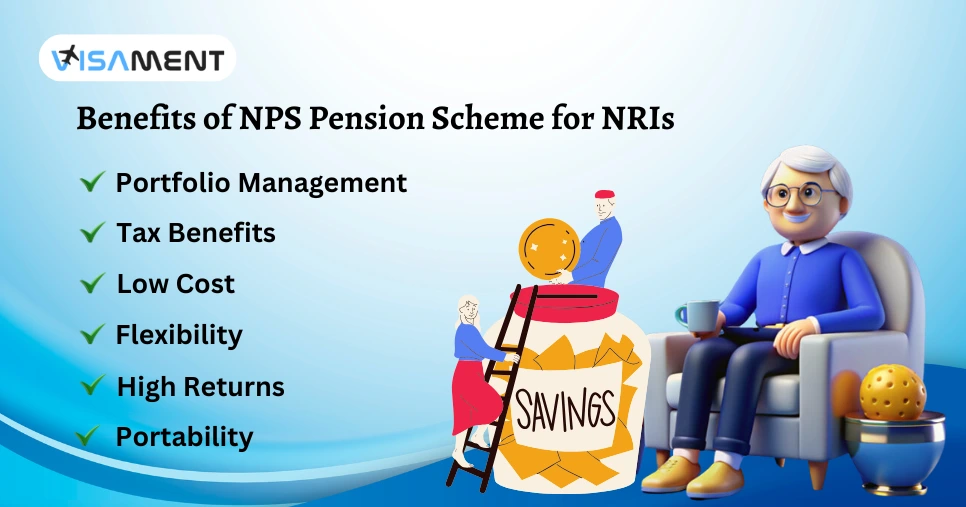

Benefits of the NPS Pension Scheme for NRIs

One of the biggest reasons many NRIs choose the National Pension Scheme is because it helps them build a retirement fund while offering flexibility and tax benefits. Along with professional fund management and market-linked returns, the scheme gives investors the freedom to choose investment options based on their financial goals. Here are some of the key benefits of the NPS for NRIs.

Portfolio Management

By choosing the Active mode option, NRI has much flexibility in the allocation of assets. In case you activate the active mode, the fund manager allocates the assets on your behalf. By the activation of this mode, the subscriber can invest in four different assets listed below:

- Government Securities: Investments are made in Central and State Government Bonds.

- Equity: Allocation of assets in stocks or related instruments on listed companies up to 75%. Also, it can be done till 50 years of age, gradually decreasing to 50% at 60 years.

- Corporate Debts: Allocation of assets done in Public Sector Units, Public Financial Institutions, and Corporate Bonds.

- Alternative Investment Funds: Allocation of assets in Real Estate Investment Trust (REIT), Mortgage-Backed Securities (MBS), and more. However, in these funds, a maximum of 5% of assets can be allocated.

Tax Benefits

Under section 80CCD (1) and the part for the overall limit of Section 80C, NRIs get tax benefits of up to Rs. 1.5 lakh. In addition, under Section 80CCD (1B) for NPS investment, they can get an extra deduction. It allows up to Rs 50000. It is in addition to the deduction done in Section 80CCD (1). Also, upon maturity at 60 years, the subscriber has the right to withdraw in a lump sum of 60% of the accumulated corpus without any tax. The remaining amount- 40% is also free from tax if it is invested in an annuity. However, as per the extant laws, money from the annuity as a pension is not tax-free.

Low Cost

With a minimum amount of Rs 500 for Tier I, you can open an NPS account. In addition, Rs. 1000 for Tier II, which is optional for NRI. Also, the second option does not offer any tax benefits to NRIs. It is more liquidity. There are no upper and lower limits set on the contribution number per year. Apart from this, the charges of fund management are also low, ranging from 0.01% to 0.1% p.a.

Flexibility

As per your financial goals and risk appetite, you can select your investment option, fund manager, and allocation of assets. In addition, you can also change between investment options and fund manager once a year. Also, for specific, reasons you are allowed to make partial withdrawals.

High Returns

The NRI pension scheme also offers market-linked returns to subscribers. It can aid you beat inflation and make a sizeable corpus over a long time. In addition, the historical average annual returns of the NPS scheme range between 9% to 15%. It generally depends on the performance of the fund manager and the allocation of assets.

Portability

Through online access, you can use your account from anywhere in the world. In addition, even after becoming a resident Indian, you can continue your NPS account.

These are the perks that you can enjoy under the National Pension Scheme for NRI. Moving ahead, let's know the available investment and withdrawal options for NRIs in NPS.

What Are the Investment and Withdrawal Options for NPS for NRIs?

Under the NPS government scheme, as an NRI, you can invest in Tier I and Tier II accounts. In this, the first one is mandatory to open. In addition, it is meant to provide retirement savings along with tax benefits. Talking about the second one is optional and does not have any tax benefits. It is a general investment with more liquidity. With this, other options for investment are listed below.

Investment Options

For the NPS account, you are provided with two options: Active and Auto Choice. As per your requirements, you can choose the one that fits your preference.

- Auto Choice: Under this option, based on the risk and age, the system automatically allocates the assets. This option consists of three life cycle funds. These are conservative (LC-25), Aggressive (LC-75,) and Moderate (LC-50). The exposure of equity in these funds began at the age of 18 from 75%, 50%, and 25%, respectively. In addition, it gradually starts decreasing at 50% to 15%, 10%, and 5% respectively.

- Active Choice: This option allows you to allocate your assets on your own. It consists of four options: government securities, corporate bonds, equity, and alternative investments. However, till the age of 50, it consists of 75% exposure of equity. In addition, it gets reduced every year by 2.5% until it reaches 50% at 60 years of age.

Apart from these two options, it also avails the option to change your investment option or fund manager once a year without any additional charge.

Withdrawal Rules

Generally, the option of withdrawing from an NPS account is available after you reach the age of 60. However, in case of premature existence, there are certain conditions applied. These are as follows:

- Attaining the Age of 60: In this case, as a lump sum without any liability of tax, you can withdraw 60% of your corpus. The remaining amount, i.e. 40%, should be used to purchase an annuity from a PFRDA-empanelled service provider giving an annuity plan. This plan provides you with a regular income for a lifetime. However, if you have less than Rs 2 Lakh, you can take out your whole amount without purchasing an annuity.

- Before Attaining the Age of 60: After 10 years of contributions, you can prematurely exit from the NPS scheme. In this scenario, only 20% of the amount you can withdraw as a lump sum. In addition, the rest amount (80%) should be used to buy an annuity. However, if you have less than Rs 1 Lakh, you can take out the whole amount without purchasing an annuity.

- Partial Withdrawal: After three years, you can withdraw 25% amount of your contributions. Withdrawals are permissible for marriage, buying a house, education, and medical treatment. You are allowed to withdraw a maximum of three times over the tenure of your NPS account, with at least a year gap in each withdrawal.

With this, in case of the death of the account holder, the nominee can get up to 100% of the accumulated corpus if the value of the fund is less than Rs 1 Lakh.

Conclusion

The National Pension Scheme for NRIs is a reliable retirement investment option for eligible Indians living abroad. With benefits like market-linked returns, tax savings, flexibility, and portability, it can help you build a secure financial future while staying connected to India.

For NRIs living in the UK, planning for the future isn't just about retirement savings. It's also important to stay informed about your residency status and documentation. If you're living in the UK, you may also find our guide on the EU Settlement Scheme helpful to understand your rights and eligibility. Likewise, if you need assistance with your Indian passport, Indian visa, or OCI card services, Visament is here to guide you through every step of the process with reliable support.

Frequently Asked Questions

Yes, investing in the National Pension Scheme is a good option for NRIs. It provides higher returns and assists them in saving some taxes which makes it the right investment plan after their retirement.

80CCD 1B is a special tax benefit offered to NRIs in India. It allows savings of up to Rs 50000 tax when contributing to the NPS for NRI.

Well, it depends on the investment goals and risk tolerance of the person. If the individual gives priority to guaranteed, low-risk returns then PPF is a good option. However, if he/she is comfortable with fluctuations in the market for higher returns, then NPS is a better choice as it provides market-linked returns with flexibility in the allocation of assets.

The NPS scheme holds drawbacks like no withdrawal till maturity, not as tax-efficient upon maturity, lock-in period, partial exemption of tax, and limited exposure of equity.

The amount you invested in buying of Annuity is free from tax. However, the annuity income that you get in the subsequent years is not tax-free. You receive tax benefits when you withdraw up to 60% of the total corpus in a lump sum.

If the corpus is less than or equal to Rs 500000 then you are allowed to do lump sum withdrawal. However, if the amount is more than Rs 500000 then 60% is paid as a lump sum, and 40% of the accumulated pension is used to buy an annuity.

Vipul Jain is the Co-Founder of Visament, a trusted platform dedicated to simplifying Indian immigration, consular, and NRI services for applicants across the globe. With extensive expertise in OCI cards, Indian passport services, visa assistance, apostille and document legalization,... See Full Bio

Categories

Table of Contents

- Can NRIs Invest in the National Pension System (NPS)?

- Key Takeaways

- What Is the National Pension Scheme (NPS)?

- As an NRI How to Invest in National Pension Scheme?

- Documents Required to Open an NPS Account for NRIs

- Eligibility Criteria for National Pension Scheme for NRIs

- Benefits of the NPS Pension Scheme for NRIs

- What Are the Investment and Withdrawal Options for NPS for NRIs?

- Conclusion

Need Help with NRI Documentation

Talk to our documentation experts for free guidance on your application.

Related Articles

Recent Post

NRI Life & Taxation

NRIs Returning to India From UAE: Tax and Investments Guide

NRIs Returning to India From UAE: Tax and Investments Guide

9 min read

Read More

NRI Life & Taxation

Tax Implications on Receiving Inheritances in India for NRIs/OCIs

Tax Implications on Receiving Inheritances in India for NRIs/OCIs

7 min read

Read More

NRI Life & Taxation

How to Replace Lost or Destroyed Birth Certificate in India?

How to Replace Lost or Destroyed Birth Certificate in India?

9 min read

Read More

NRI Life & Taxation

NRIs Returning to India from the Canada: Tax and Investment Guide

NRIs Returning to India from the Canada: Tax and Investment Guide

9 min read

Read More